Popüler aramalar

Ticari karayolu taşımacılığının karbonsuzlaşmasını şekillendiren güçleri ve geçişi yönetmek için mevcut desteği anlamak.

Matthias Maedge, Eurowag Ticari Karayolu Taşımacılığı Karbonsuzlaştırma Başkan Yardımcısı

Eurowag kısa süre önce Avrupa genelindeki ticari karayolu taşımacılığı (TKT) müşterileri arasında, sektörün karbonsuzlaşmasını etkileyen başlıca engelleri ve motivasyonları inceleyen bir anket gerçekleştirdi. Başlıca bulgulardan ikisi, müşterilerimizin:

Bu görüşlerin, TKT şirketlerinin kendi müşterilerinden – onları emisyon azaltımı sağlamaya iten – karşılaştığı baskıyı yansıttığını biliyoruz. Çoğu durumda, bu durum, daha büyük nakliyecilerin ve taşımacılık alıcılarının değer zincirindeki dolaylı emisyonları (Kapsam 3) raporlamasını gerektiren Kurumsal Sürdürülebilirlik Raporlama Direktifi (CSRD) tarafından yönlendiriliyor. Bu da, nakliyeciler kombine taşımacılık ve yurt içi yük hareketleri için ağırlıklı olarak karayolu taşımacılığı hizmetlerine güvendiğinden, TKT şirketleri üzerinde kendi doğrudan (Kapsam 1) emisyonlarını azaltmaları için baskı oluşturuyor.

Eurowag bu konuya büyük bir tutkuyla önem veriyor. Sektörün karbonsuzlaşmasına sıkı sıkıya bağlıyız – çünkü gezegenin sağlığı için gerekli – ve bu değişime öncülük etme rolünü üstlendik. Aynı zamanda, müşterilerimizin uzun vadeli rekabet gücünü korumaya ve gelişen bir TKT sektörü sağlamaya da aynı derecede bağlıyız – ki bu olmadan hiçbir modern ekonomi ayakta kalamaz.

Müşterilerimizle her gün konuşarak, başka iki önemli şeyi daha biliyoruz:

Birincisi, düzenleyici çerçeve birçok TKT şirketi için kafa karıştırıcı. İkincisi ise, düşük emisyonlu araçlara ve yakıtlara geçişin önündeki engeller, zaten baskı altında olan ve dar kar marjlarıyla çalışan şirketler için göz korkutucu.

Bu blog, bu iki noktayı da ele almak üzere tasarlandı – şunları yapacak:

Tüm sektörümüz için zorluklardan biri, karbonsuzlaşma söz konusu olduğunda işletme ortamını şekillendiren birkaç Avrupa mevzuatının bulunmasıdır. İşte en önemlileri:

Bu, iki ilgili soruyu akla getiriyor: Bu mevzuat istenen etkiyi yaratıyor mu? Avrupa düzeyinde hedeflenen amaçlara ulaşma yolunda mıyız?

Bu iki sorunun da kısa cevabı 'hayır'.

Mayıs 2025'te Avrupa Komisyonu, "ağır hizmet karayolu taşıtlarının teknolojik ve pazar olgunluğu" hakkında bir Tebliğ yayımladı (COM/2025/260 final).

Bu, CRT sektöründe sıfır emisyonlu araçlara geçiş konusunda mevcut durumumuzu gösteren, faydalı ama pek de cesaret verici olmayan bir anlık görüntüydü. 2024 yılında şunları ortaya koydu:

Bu nedenle bu, önceki yıllara göre önemli bir büyüme gösteriyor, ancak sıfır emisyonlu kamyonların payı son derece küçük kalmaya devam ediyor.

Mevcut veriler, mevcut durumu ortaya koyuyor. Son 15 yılda karayolu taşımacılığı hacimleri %20 artarken, sera gazı emisyonları da arttı – ancak daha yavaş. Bir miktar ilerleme kaydediyoruz, ancak yeterli değil:

Ancak kamyon üreticileri, sıfır emisyonlu segmentin genişlemesi konusunda iyimser. Onlar Avrupa Komisyonu'na bildirdi ki, 2030 yılına kadar her üç yeni ağır hizmet aracından birinin sıfır emisyonlu olmasının beklenebileceğini – sıfır emisyonlu araç filosunu 410.000-600.000 araca (HDV filosunun %5-9'u) çıkararak. Ancak, Avrupa Komisyonu Başkanı Ursula von der Leyen'e yazdıkları son bir mektupta şüphelerini dile getirmeye başladılar ve "rotayı düzeltme" çağrısında bulundular.

Komisyon bile bu tahminler konusunda şüpheci. Bu Tebliğ şunu söyledi: "Sıfır emisyonlu ağır hizmet araçlarının fiyatlarının önümüzdeki yıllarda düşmesi ve TCO'nun [Toplam Sahip Olma Maliyeti] önemli ölçüde daha uygun hale gelmesi beklense de, bu, küçük kar marjları, yatırım yapacak sermayesi kısıtlı birçok KOBİ işletmecisi ve 2025'te sıfır emisyonlu araçların çok küçük bir paya sahip olduğu bir pazarda çok kısa bir sürede keskin bir pazar artışı olacaktır."

Eurowag olarak görüşümüz, Komisyon'un beklenen pazar projeksiyonları konusunda şüpheci olmakta haklı olduğu, ancak bunların OEM'lerin geçişi hızlandırmak için üzerindeki baskıyı yansıttığı yönündedir. Ve bunlar abartılı tahminler olsa bile, değişimin geldiği – ve hızla geldiği – şüphe götürmez.

Eurowag'ın 30.000'den fazla aktif karayolu taşımacılığı şirketi müşterisi var, so it is our business to understand the pressure they are under and the challenges they are facing. For us, the fact that the take-up of zero-emissions trucks and the growth of the necessary infrastructure has been slower than planned is no surprise – because transitioning to alternative energies is not an easy decision for most CRT companies to make.

We know how competitive and price sensitive the industry is. We understand how big a decision every truck purchase is, and how carefully the TCO is calculated. We therefore appreciate how tough it is for most firms to consider an eTruck when the purchase price is more than twice as high as a diesel truck (let alone a hydrogen truck, which is even more expensive than that).

We also understand the concerns over the limited recharging / refuelling network, especially on long-haul routes.

As always, some do and some don’t – but not enough do, which is why Eurowag is educating policy-makers across Europe so that they understand the realities of our industry. Our objective is not to try to slow down the decarbonisation agenda. On the contrary, our objective is to champion the interests of our customers by helping policy-makers formulate policies which have a realistic chance of working in the real world.

Most importantly, we are emphasising the challenges created by policy incoherence. As an example, while RED III and CountEmissions EU propose a life cycle approach to emissions, the CO₂ Emission Standards for Heavy-Duty Vehicles focuses solely on tailpipe emissions, effectively closing the door on alternative fuels. This inconsistency conflicts with the principle of technology neutrality and could slow progress on decarbonisation. The European Commission must also refrain from picking winners and losers and allow market-driven solutions to compete on equal terms.

These issues are a particular threat in Central & Eastern Europe (CEE), which plays a leading role in international road transport. Indeed, four of the top five European countries for international freight transport are in CEE, representing about 250,000 businesses.

In March this year, Eurowag took a leading part in the Fuel Congress 2025 in Warsaw, at which representatives from across CEE signed a joint Call for Action to the European Commission. The Call for Action has now been endorsed by more than 30 organisations across Europe and sent to Commission President Ursula von der Leyen. Eurowag is also actively working with Fleet Cards Europe (FCE), a Brussels-based trade organisation representing the fleet card business which is in very close touch with road transport companies and serves their interests. FCE is part of the Network for Sustainable Mobility (NSM), an informal coalition of like-minded stakeholders which is calling on the European Commission to adapt the legal framework.

Amongst other policy priorities, Eurowag is pushing for:

If you would be interested to hear more about Eurowag’s advocacy work, or support us in this area, please get in touch.

Amid military conflicts and rising energy supply ambiguities, over the last few months, the conversation has been building around the future of the EU’s Green Deal and the recently presented Clean Industrial Deal. In certain areas, some detect a change in tone from the European Commission – a shift towards greater pragmatism, even a dialling down of ambition.

But the direction of travel is already set for the transport sector. The legislation is already in place and the deadlines are fixed. OEMs are mobilising to meet their own targets.

Companies are fooling themselves if they believe that the decarbonisation wave will miss them. It is coming, and it will change the entire sector.

Those who respond now, by adopting electric vehicles and replacing diesel with decarbonised fuels, acting before they are left with no choice, will gain a competitive advantage in the short-term and protect their long-term viability in the longer-term.

Those who don’t respond are taking a huge risk.

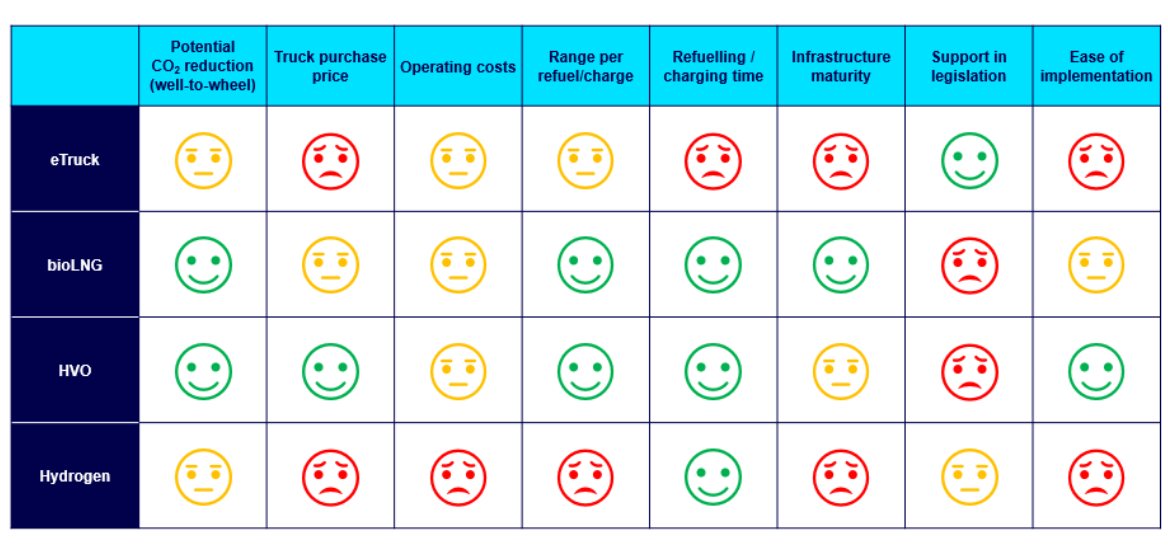

Different technologies and fuels are suitable for different types of transport – urban and regional transport are very different from long-haul international trucking – and the right choice for each business will depend on multiple factors.

Here are the four options when it comes to alternative fuels:

1. HVO (Hydrotreated Vegetable Oil) is a drop-in fuel, which means CRT companies can start reducing their CO2 emissions with their current fleet and use it without any restrictions in diesel engines. The preferred feedstocks for producing HVO are either animal fat residues or used cooking oils, which can deliver a CO2 reduction of up to 90% on a well-to-wheel basis.

HVO is the fastest and easiest solution to deliver a significant emissions reduction. Right now, the price is 10-25% higher than diesel, but it is gaining popularity while diesel prices will gradually go up.

2. Liquefied biomethane and compressed biomethaneoffer up to a 100% CO₂ reduction compared to conventional diesel. Biomethane is making strong inroads in heavy-duty transportation, available at over 30% of European LNG refuelling stations – and growing all the time.

BioLNG trucks can also do more than 1,500 km on a single tank, and switching to bioLNG can reduce operational costs by over 30% compared to diesel. It is even cheaper than diesel in Germany, for example, because of the greenhouse gas quota system. More countries are expected to introduce such greenhouse gas quotas to comply with the REDIII objectives.

3. eTrucks are favoured by EU policy-makers because they are zero tailpipe emissions, and there are around 40 eTruck models already available on the market. With fewer moving parts, there are also maintenance savings available.

As the e-charging network develops across Europe, and as subsidies become available in more countries, eTrucks will become a more and more viable option for CRT companies – particularly those focused on last-mile delivery, regional transport and point-to-point regular medium- to long-haul routes.

4. Hydrogen is also popular in Brussels for the same reason: it is a zero tailpipe emission technology. Hydrogen trucks can also be refuelled in about the same time it takes to fill up with diesel, offering a significant advantage over electromobility.

Hydrogen will, in time, have a major impact on the industry, particularly as its availability and the refuelling network expands. However, it is still in the early stages of development – and therefore prohibitively expensive right now.

There are a variety of ways in which Eurowag is supporting customers to manage the decarbonisation transition:

Decarbonisation as a Service

More and more CRT companies are looking for a trusted, informed partner to help them navigate this transformation and stay ahead of compliance requirements – but also to maintain their competitive edge in a shifting marketplace. Eurowag’s Decarbonisation as a Service (DaaS) offer is a holistic approach to helping customers transition to net-zero and stay relevant in business.

This includes:

Eurowag’s acceptance network for alternative fuels is continually expanding to meet the growing demand. Right now, it includes:

In 2024, Eurowag became the first eMobility Service Provider in Europe entirely focused on the CRT industry. As well as offering CRT companies access to a comprehensive network of electric charging stations for trucks and vans across Europe, our eMobility services include:

We are also continuing to grow the dedicated heavy-duty vehicle charging network and support customers with integrated fleet and charging services, including in depots and on-route co-financing and commercialisation (semi-public access).

The importance of data is not, of course, restricted to eMobility. Across the full range of alternative fuels, we go beyond infrastructure access to deliver what truly drives change: reliable sustainability data that empowers smarter decisions.

Our platform gives fleet operators and logistics companies the ability to track emissions in real time, assess the true impact of route and fuel choices, and report with confidence – backed by accurate, independently verified data. From meeting CO₂ reporting standards to demonstrating progress towards customers’ sustainability goals, Eurowag helps make every charge, refill, and route a step toward measurable decarbonisation.

The CRT sector is entering a decisive phase. The legislation is in place, the infrastructure is expanding, and the expectations from partners, policymakers and end-customers are rising fast. The direction of travel is clear: the future belongs to alternative energies.

This is no longer just about avoiding risk. Transitioning early can reduce costs, unlock new business opportunities and signal leadership in a low-carbon economy. And the sooner you move, the stronger your position will be in tomorrow’s market.

Don’t wait for the change to be forced upon you. Let Eurowag help you get ahead of it.

Schedule a today – and take your first step toward a cleaner, more competitive future.